May 31, 2023

Our series on the current state of the economy started with a discussion of America’s labor shortage, a significant driver in price increases and inflation, followed by commentary on the relative benefits of a banking crisis to slow the American consumer. Both of these topics lead to the question of whether a soft landing is possible.

In the past several months, the U.S. consumer has been shifting away from spending on goods and back toward services, which is traditionally the primary driver of the U.S. economy. If you remember from our post from this time last year, goods and services spending was significantly disrupted by the pandemic, which created ripple effects throughout our consumer-driven economy.

When forced to stay home in 2020, we spent more on goods. Then in 2021, shortages led to a ramp up of manufacturing to meet demand, followed last year by a glut of inventory.

Now in 2023, the consumer has pulled back from goods spending. In one example, Thor Industries, owner of a large portfolio of RV brands, experienced a 39.6% drop in sales from the prior year. The next logical step is a slowdown in manufacturing, which was one of the primary drivers that helped us avoid a recession over the last 18 months. This slowdown, paired with falling commodities prices like crude oil (gas down 30% in the last year), led many down the path of doom and gloom.

Data: U.S. Energy Information Administration; Chart: Axios Visuals

But we’d like to turn that frown upside down…

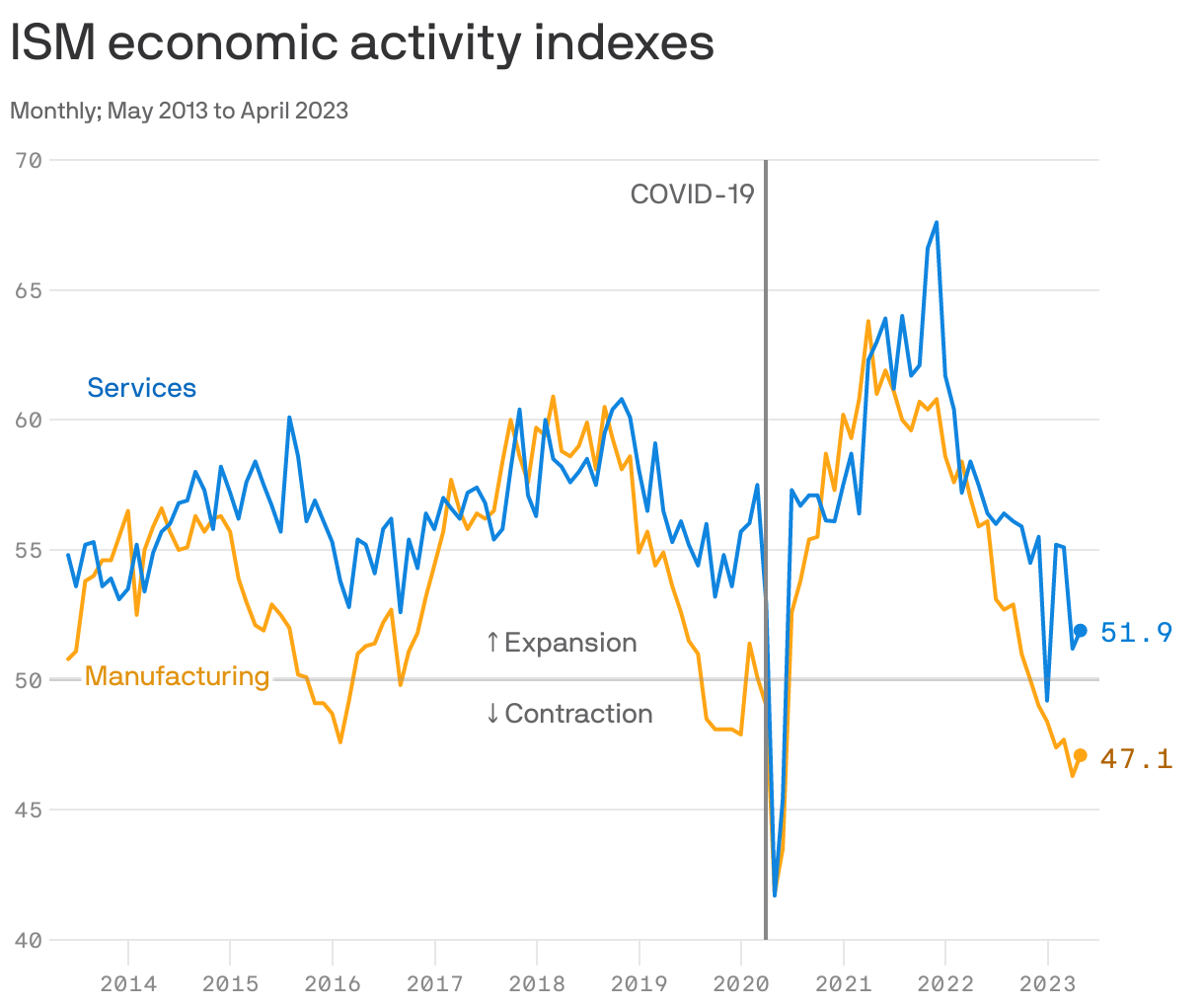

Data from the Institute for Supply Management’s survey of manufacturing and services activity for April confirm the growing divergence between manufacturing and services spending, with services accounting for over 70% of total consumer spending.

Data: FactSet; Chart: Axios Visuals

As confirmed by ISM and in the chart above, manufacturing is shrinking, while services spending shows continued expansion (contraction is represented as less than 50, expansion is above 50). Services spending represents travel, money lending, professional services, haircuts, restaurant meals and more; it is a key driver of employment but especially lower-wage employment. This supports the spending cycle and may just be enough to avoid a manufacturing hangover for the economy.

It’s not all rosy, but it’s a much rosier than I anticipated given the speed and consistency of the Fed’s interest rate increases.

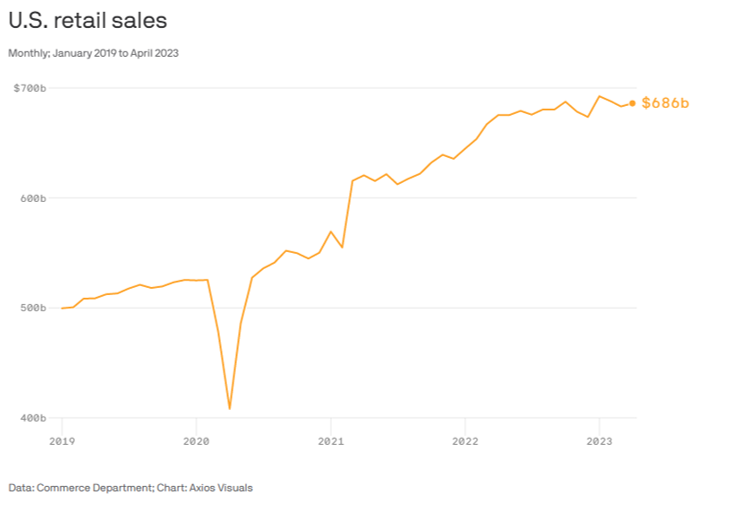

Despite rate increases, the U.S. consumer has continued to spend, but differently from last year. Retail spending data published last week show an uptick in spending after several months of declines. But when you zoom out, it appears that most people are actually spending less than they were in 2022.

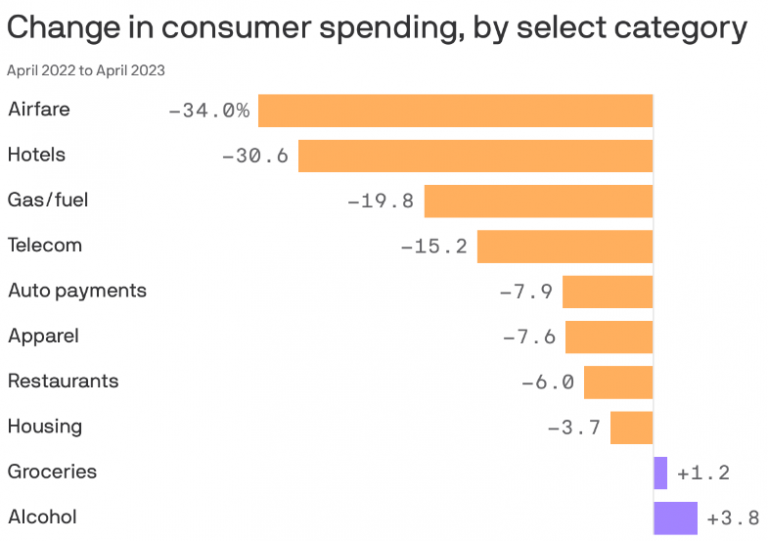

This could just be the dream Jay Powell has been waiting for…a soft landing where we keep our jobs and spend a bit less, bringing down inflation pressure without triggering a recession. If that is possible, it would look like the chart below; where we travel less and sit at home cooking and drinking more.

Data: Morning Consult; Chart: Axios Visuals

Morning Consult breaks down spending growth in goods and services categories over the prior year, summarized in the chart above and takeaways below:

- Spending on vacations declined from 2022

- Households tapped into savings, while real incomes increased

- Core inflation is still too high and monthly inflation ticked up after 9 months of declines

One thing to note in the Morning Consult data—they use “trimmed means” to ignore the highest spenders who might skew aggregates that the overall spending data includes (sorry Bezos).

What does that mean for a soft landing? Even though it’s never happened before, it might just be within reach. The economy is cooling off after sustained strength, but not in a precipitous way. After spending in 2022 like there was no tomorrow, tomorrow has come, and so far, it’s feeling subdued and steady. Just like Jay’s dream.