June 2, 2022

We are in the midst of an extreme dislocation between spending on goods and services brought on by the Covid-19 pandemic—that much is fact. But three questions remain up for debate: How extreme is the change? How will we know when spending has fully recovered? And where will spending go in the near-term, based on current trends and what has happened so far?

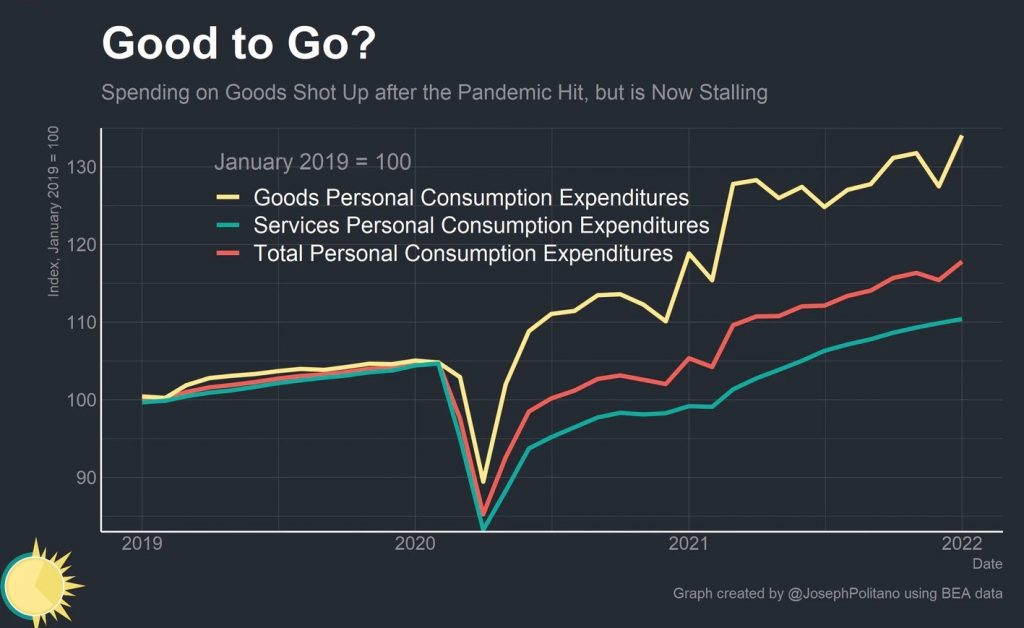

Let’s start with how much displacement there has been in consumption overall and, more specifically, the difference in spending on goods vs. services. The chart below, courtesy of Joseph Politano from the Bureau of Labor Statistics, measures the change in consumer spending since January 2019. Indexing to 2019 concludes that goods spending recovered to pre-pandemic spending after several months while services spending recovered in May 2021. With this methodology, total spending recovered January 2021.

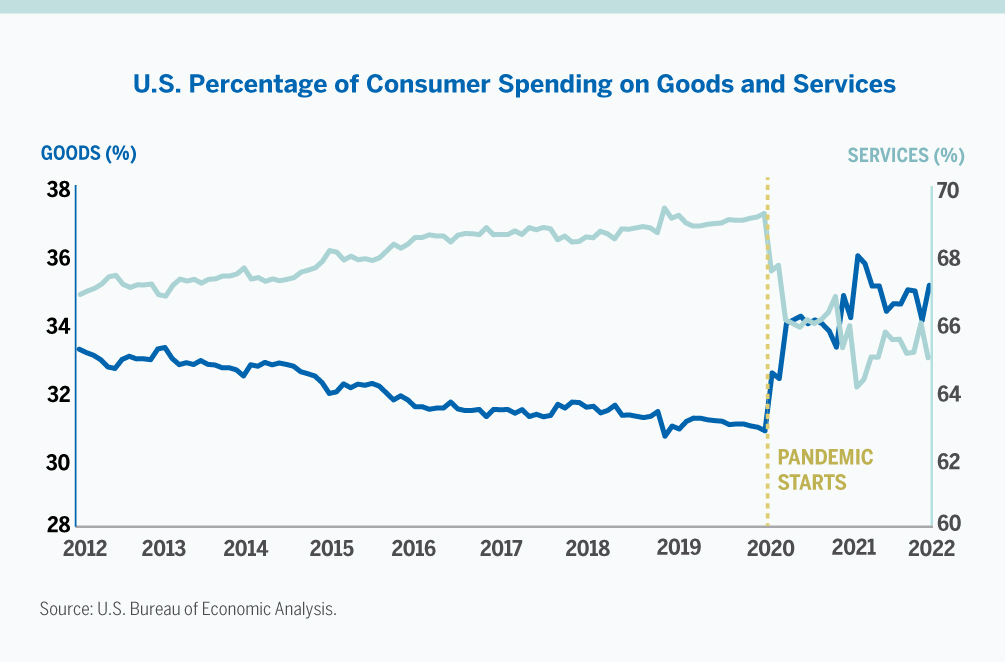

The challenge with indexing to 2019 is that it severely underestimates the value of services spending as a portion of total consumer spending. The chart below based on data from the Bureau of Economic Analysis illustrates how services spending represents nearly double the amount of spending on goods in the US economy and just how far away we are from the pre-pandemic “normal.”

Finally, my favorite chart for telling this story. Thank you to the Oregon Office of Economic Analysis for giving us a way to see spending in terms of real dollars, the relationship of goods to service spending, and perhaps most importantly, spending relative to pre-Covid trendlines.

Why do we need all three?

Weighting to time zero of January 2019 looks at the relative change, but not the overall change in spending—how many dollars were lost and how many need to be replaced, not just the relationship between goods and services.

The pre-Covid trendline indicates how much consumer spending was anticipated to rise given typical, expected projections. This is how we plan manufacturing timelines, supply chains, and how we keep essential goods like baby formula on the shelf. We see in this chart that goods are 19 percent over the trendline (after inflation it remains 8 percent above trend), surely an unsustainable level on its own; it also shows that services spending has failed to recover to what we would reasonably anticipate today.

These differences have significant downstream implications for our economy, especially transportation, manufacturing, and retail; but let’s not forget real estate.

Manufacturers ramped up production to meet consumers’ insatiable need to buy, we’re now producing more and trucking/shipping more. We need more warehouse space and many retailers’ stores that pre-Covid were struggling are now finally in the black.

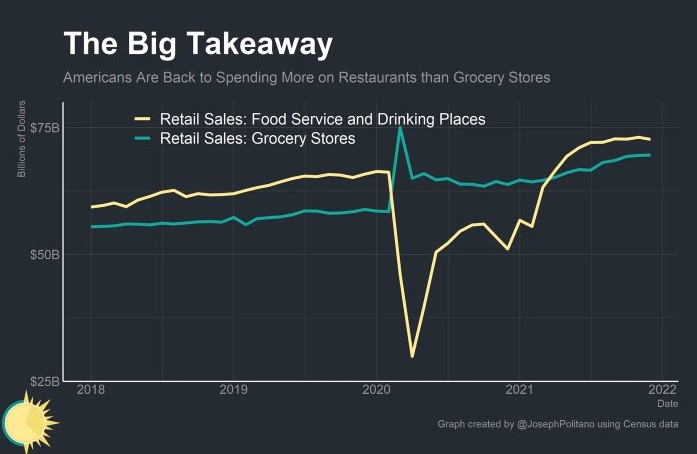

What’s next and when will spending revert? Food spending offers us a clue.

BONUS CHART

I love discussing the relationship of spending on food at home vs. food away from home; a.k.a. share-of-stomach. It took nearly two years for consumers to return to the pre-Covid relationship of spending more on food away from home than food at home. Pre-Covid (full year 2018), Americans spent 54 percent of all food dollars on restaurants. In 2020 we saw an 11 percent shift in market share to food at home. Today Americans are spending far more than the pre-Covid projection on food spending overall, as described above, but if food spending is any indication of our desire to return to our pre-Covid lives, then expect goods spending to moderate in turn.

I love discussing the relationship of spending on food at home vs. food away from home; a.k.a. share-of-stomach. It took nearly two years for consumers to return to the pre-Covid relationship of spending more on food away from home than food at home. Pre-Covid (full year 2018), Americans spent 54 percent of all food dollars on restaurants. In 2020 we saw an 11 percent shift in market share to food at home. Today Americans are spending far more than the pre-Covid projection on food spending overall, as described above, but if food spending is any indication of our desire to return to our pre-Covid lives, then expect goods spending to moderate in turn.

What does this reversion mean for commercial real estate?

We’ve ramped up production on goods to meet consumer demand, but consumers have started to demand different things, and we are on the cusp of them wanting less overall. When manufacturing remains elevated, our risk of recession is tempered, but that will only go on for so long. Consumers are on the precipice of a reduction goods spending that will have ripple effects on manufacturing and transportation. The need for excess supply chain real estate will vanish for many established operators (even Amazon has 10 million sq. ft. of excess space).

17 of the 20 largest retailers in America remained open during lockdowns. They saw large portions of under-performing stores suddenly turn positive. Over the next six to nine months when consumer spending pulls back, we will see which stores will languish and how many will close. This is healthy and necessary—we need to return to more sustainable spending on goods in order to fuel the services sector long-term.

The next phase of pandemic recovery is where we see who has been disciplined, and who has been swimming naked.