March 25, 2024

A year ago [has it been that long already?] we commenced a series on the state of the economy. We started with examining America’s labor shortage, a significant driver of price increases for goods, followed by our thoughts on whether stresses on regional banks could benefit the American consumer by putting a pinch on spending. Those two topics led to the ultimate question of whether a soft landing was possible.

If the most-used term of 2020 was “social-distancing,” then surely the equivalent for last year was “soft landing.”

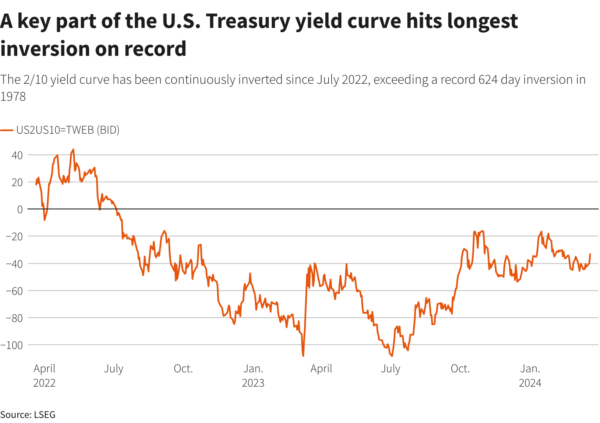

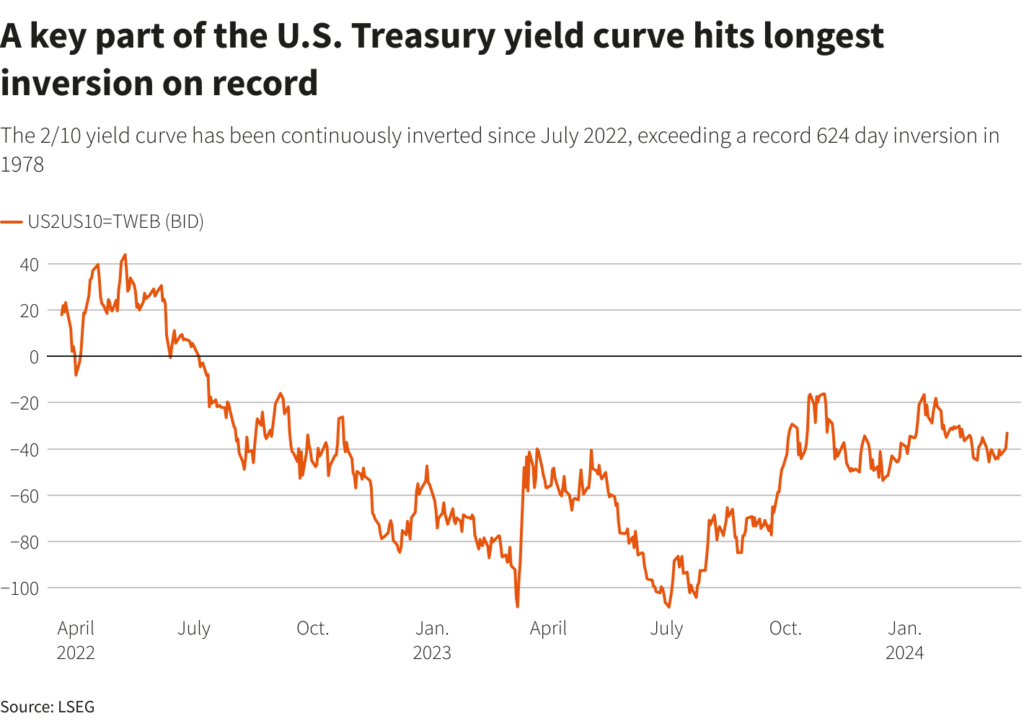

Since July 2022, many indicators—especially the never-been-wrong, inverted yield curve—have portended an upcoming recession. (In fact, the yield curve has been inverted for so long that it has now beaten the 624-day record set in 1978.)

Reuters Graphics

The inverted yield curve is a drag on the economy in and of itself because higher rates on shorter-term risk make it more expensive both for today’s consumer and for commercial loans, all while simultaneously discouraging long-term risk, since longer-duration investments are at lower rates.

During our present business cycle, we’ve had the opportunity to see many instances where the typical indicators aren’t applying, at least not yet. For the inverted yield curve, part of the lagging impact is due to increased savings from pandemic-era spending. While this is waning and consumer credit continues to tick up, the American consumer was more insulated against inflation and the resulting rise in interest rates than they have been in prior cycles due to increased savings from pandemic stimulus.

And that resilience and cushion led us to today’s soft landing. Given that many economic metrics focus on the rearview mirror, it can be hard to pinpoint where we are until we’ve passed the mark. In this case, I believe we are past the point of the soft landing. The plane has been on the ground for the last six months.

Remember the Hot Labor Summer of 2023? Turns out it was also the No Deal Summer. This time I’ll be the one to take a look in the rearview mirror six months past. August was the point at which rising cap rates on commercial transactions, combined with the quick rise of interest rates, resulted in the inability to get almost anything over the finish line, with very few exceptions.

With that behind us, what can we look forward to?

For the last several months, I’ve been looking for cracks. Something that would point to the economy getting materially better or worse. We continue to see unemployment exceptionally low, at 3.9% for February 2024.

Inflation has eased but is by no means over, and of course, it matters which measure of inflation you’re referencing. We tend to think of inflation as CPI, the consumer price index, but the Federal Reserve targets PCE, the personal consumption expenditures price index. There are numerous differences between the two measures, but for our purposes, the difference between these two can contribute to the difficult decisions behind the timing of changes to the Fed funds rate. We saw this recently with the Fed’s decision to maintain current interest rate targets this month and reduce its target of cuts in 2024 from four to three.

This leaves us in a situation where we have better news from an inflation standpoint with a clear peak in February 2022 followed by (choppy) lower inflation from that point. The gap between CPI and PCE will continue to give us a bit of whiplash between what consumers are experiencing and where the Fed will feel comfortable enough to believe we are on a sustainable path long enough to cut rates.

That leaves us in a state of stability. Many of the largest capital allocators are looking at their dry powder and are getting antsy to deploy, especially in commercial real estate.

While we would never paint commercial real estate with a broad brush, the office sector, and a small segment of high vacancy buildings within the office sector, have served to drag down views of commercial real estate as a whole. Too many institutional investors pinned their hopes on always-in-favor assets in target markets, only to see those assets sour. This is no different than the fallout from the so-called “retail apocalypse” when investors found themselves with super-regional centers that were no longer all that super or regional

This leaves us in a place where there is a strong desire to deploy capital, especially when assets can be purchased without the high-interest financing available today. The squeeze? What owner wants to sell in this high-cap rate environment, especially if they have more time on their existing low-interest loans? Nearly none. If we continue to stay in the current stable economic state, we will continue to see very little deal flow.

This will change when things either get better or worse. Worse would mean we continue our short-term soft landing, leading into an interest rate-induced recession, prompting the Fed to cut rates and kick-start (distressed?) transactions.

Better is more difficult to quantify. It indicates that CPI is low enough, long enough to give the Fed confidence that it can lower interest rates without triggering a recession and overheating the economy, which could kick off another round of inflation, as the country experienced in 1980 [Note that the inflation cycle from peak to peak was just over six years, from November 1974 to January 1980; that is a very long time to wait to be wrong].

Better or worse, this will take longer than we want and longer than I have patience for most days. Where many (most?) economists are looking at Fed rate cuts in June and the messaged three rate cuts in 2024, I will take the over. I believe we will be lucky to see a rate cut in the Fall and I wouldn’t be surprised to not have one in 2024 at all.

I hope I’m wrong.