We’re days away from Christmas, the busiest days for retail spending are upon us, and even for those of us that track this data regularly, there are conflicting indicators left and right. Will the consumer continue to show up with overwhelming spending this season? Will out-of-stocks and inflation concerns create a headwind on spending?

While spending on services has recently surpassed pre-pandemic levels after 15-months, Americans continue to spend significantly more on goods than ever before. As we touched on in the first article in this series, this increased spending on goods—among other trends—has led us to the supply chain crunch we’re in today.

How has this goods spending increase (and the corresponding reduced spending on services) impacted retailers and their demand for real estate?

Let’s look at both the retailer’s and landlord’s perspectives.

It’s obvious that non-essential retailers suffered most in 2020, but an interesting pattern emerged where some retailers utilized the forced closures as an opportunity to evaluate which stores they would reopen following lockdown; a get-out-of-jail-free card for underperforming stores. This led to an interesting outcome for mall-based owners, where their rent and sales per square foot averages shot up because weaker tenants vacated (denominators can be win-lose sometimes).

On the shopping center side, there was significant sales consolidation among the largest retailers, due in part to supply-chain constraints and “out of stock” items. It’s easy to see why this would favor the likes of Walmart and Target: Why go all over town to fill your basket when you’re concerned about contracting a deadly virus?

Consumers changed their pattern from using six different channels for food-at-home to one to two stores. Shoppers weren’t just focused on whether a retailer carried a particular SKU; they were basing their choices on the perceived likelihood that the item would be available on the shelf or online.

This, again, favored mass-market operators. In March 2020, PetSmart’s supply chain included not just PetSmart-branded stores, but also its 70% stake in Chewy.com, making the combined PetSmart/Chewy enterprise the clear leader in pet supplies in the U.S.

Internally at PetSmart, it’s common to hear the refrain “we got more than our fair share” when it comes to being prioritized by suppliers. What does that mean for the consumer? If you need your Blue Buffalo dog food and your local or regional store has bare shelves, but the PetSmart is full, now you’re a PetSmart customer.

It’s no surprise that when the government shuts down your competition you do well. But there’s a consequence to that success for essential retailers. Where non-essential retailers rationalized their fleet over the last 18-months, many essential retailers saw their least productive stores bounce back from the edge of oblivion. Will that continue?

The answer comes down to fresh.

Our shopping patterns, especially in terms of store format, size, number of stores and market penetration, largely come down to the immediacy of the product. But while it might sound counterintuitive, temperature is a pretty good proxy for immediacy. I’m not using a metaphor here: Consumers are more likely to urgently need something that is cold, like milk or eggs, as opposed to a coffee maker from Bed Bath & Beyond.

You could count up the number of cold cases within those four walls and make some pretty solid predictions about the sales and traffic trajectory of that operator, at least for now.

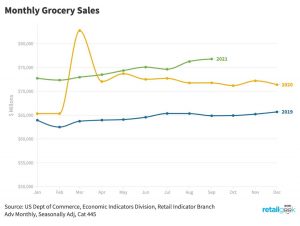

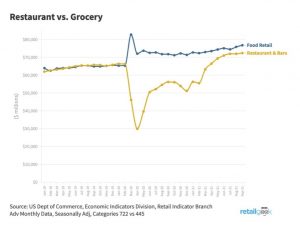

Food away from home has suffered, and we’ve seen exhaustive news coverage and industry discussion about the tremendous increase in food-at-home that was part and parcel of that shift. . What gets less coverage is just how much more we’re spending on food at home over a sustained basis, even after restrictions have been lifted. This may look like pandemic preferences are becoming more permanent, but we think it’s also likely a larger pie for overall food spending, which will persist even after we’ve gone back to regular restaurant dining.

Because of the increase in spending, many of those bottom-performing grocery stores are now sustainable, especially if they are in markets with improving demographic trends in terms of in-migration and household formation.

But we didn’t just change the basket of items and the retailers we shopped, we also changed whether we bought online vs. in store, and we chose between pickup and delivery. Americans are 50% more likely to pick up a temperature-controlled order than an ambient one. That’s good news not only for grocery retailers that haven’t yet made eCommerce delivery profitable, but it’s also good for the small shop tenants that rely on anchor traffic to boost their sales. Finally, it’s good for the landlord.

Because landlords have more power than they’ve had in over a decade.

If you were at ICSC in Vegas last week, you might have thought it was 2006 again. I heard the word “unprecedented” tossed around enough times to make me feel that I was surrounded by goldfish with no memories.

What we’re seeing is the result of historically low supply delivered over the last 10 years, coupled with the culling of weaker credit tenants, and sustained increased retail spending. That’s led us to a point where—I never thought I’d be writing this—many retail landlords can shift from being focused primarily on filling vacancies, to being focused on pushing rents.

An important caveat is that the shopping center market is highly fragmented. The ability to increase rents will be reserved for the most diligent institutional real estate owners that have responsibly recycled their capital out of lower-quality assets, leaving them with the best of the best shopping centers that can demand rent increases.

While I’m concerned about the exuberance, I think these tailwinds persist for institutional landlords well into 2022 and possibly 2023.

What could go wrong? Here’s what we’re most concerned about for retail real estate in 2022.

Both sales and profitability have increased for many essential retailers. However, due to an increasing percentage of their sales moving online, they need to rebalance the fleet in terms of the fulfillment of goods between their retail and industrial assets.

They will consider whether the sales that move online are more likely to be fulfilled via ship-to-home (like Kroger’s Ocado) or via pickup (like Target’s Sortation Centers) and if customers will maintain a separation of ambient vs. temperature-controlled being the driver of pickup vs. delivery.

How about the offering? Are the items within the store and the format of the store still relevant for a customer that shops with significantly changed frequency, channel, and location as they shopped 15 years ago? How many items that existed because of “convenience” aren’t as convenient when Amazon can get it to you in a few hours?

If the format and SKUs are still relevant, are the stores located in the right MSAs as population continues to shift to the Sunbelt? And if the SKUs, format and MSA locations are all correct, do we still need the same number of stores to “cover” a market? Or can we consolidate more stores, use dark stores for fulfillment, or recapture more selling space for packing/picking space in average-performing stores?

Working in the retailer’s favor is decades of remaining term at nearly flat rents and an inflationary environment that makes that rent increase largely disappear. But for those of you that love health-ratios, be warned: The largest contributor to store profitability is labor.

Inflation could (and should) lead to increased wages for retail workers, the largest job category in America, impacting retailers’ profitability and, in turn, their ability to invest in adapting their stores and supply chain to the changing consumer. That may be the turning point for essential retailers that haven’t had to rationalize their fleet.

I received quite a bit of outreach when CVS announced they’re closing 900 stores.

With a fleet of nearly 10,000 stores, and spread over three-years, that’s around 3% of stores closing each year. The bottom 3% located in the weakest markets with the lowest chance of future success.

Culling is healthy and necessary. It’s not a surprise, it’s good business.