Retail REITs: Grocery Windfall Well-Timed as COVID-19 Accelerates Shift Online;

WeinPlus Conference Call Takeaways

Todd M. Thomas, CFA / (917) 368-2286 / tthomas@key.com

Jordan Sadler / (917) 368-2280 / jsadler@key.com

Ravi Vaidya, CFA / (917) 368-2373 / ravi.vaidya@key.com

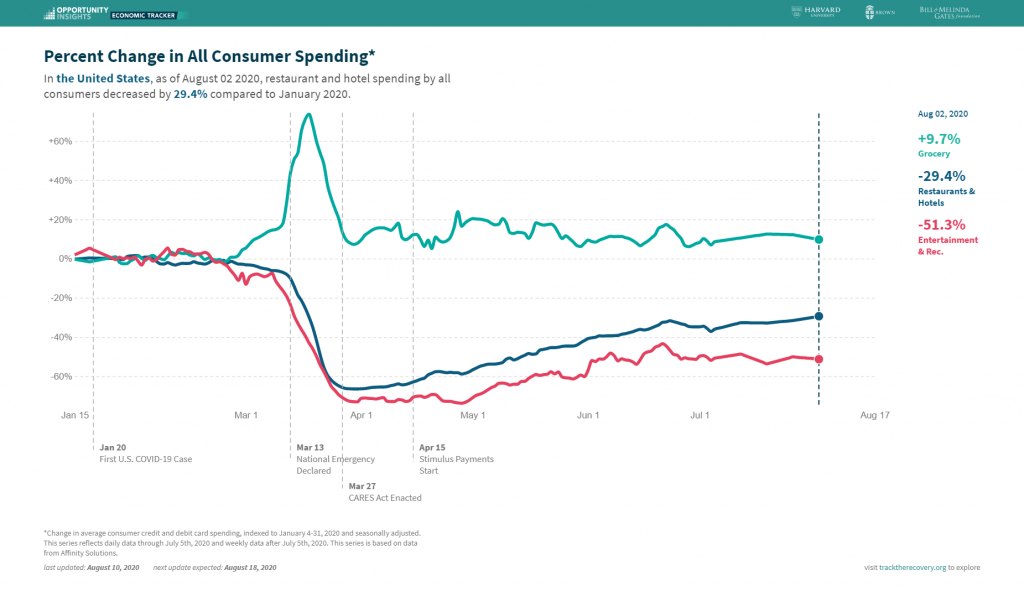

While the ongoing pandemic has created significant headwinds across the retail real estate industry, grocery has been a clear standout to the upside. This has important implications for retail property owners, which we discussed last week with Rachel Elias Wein, Founder and CEO of WeinPlus. Unsurprisingly, grocers are seeing a significant increase in demand and are better positioned to adapt to the evolving landscape (i.e., online, fulfillment) than they were pre-pandemic. We look for grocers and food retailers to accelerate investments in digital capabilities, fulfillment, and in-store remodels; moreover, we suspect the risk of store closures may be less likely in the near term than they were pre-pandemic, and many retailers may look to expand footprints in order to capture share of the increase in grocery spend.

We hosted a call with Rachel Elias Wein, Founder and CEO of WeinPlus, to discuss the changing grocery landscape and the impact

on retail real estate. Key takeaways from the call are below:

Food sales shift back to the dinner table; suburbanization wave may have legs. After many years of increasing consumer spend on food away from home (54% share in 2019), it is forecast that as much as $200B could leave restaurants, with as much as $100B redirected to grocers and other food retailers; consumers pocket the remaining $100B, with food-at-home costs being an estimated 50% less expensive. The longer the pandemic persists, the greater the windfall for the grocery industry, and the greater the pain may be for restaurants. Notably, Ms. Wein believes the increase in work-from-home trends along with population outflows from urban/city centers to the suburbs could have a meaningful impact on shopping center spend, particularly in second- and third-tier cities (e.g., Nashville, Tampa, Phoenix, etc.).

What does this mean for brick-and-mortar? These quick and sudden changes have important implications for the grocery industry, which acts as an important anchor (or shadow anchor) for a high percentage of retail properties. Pre-COVID-19, grocers were investing in existing stores, new stores, fulfillment, technology/payments, and people, though retailers had to be judicious with capital given constraints. Given the increase in sales and cash flow, grocers have an opportunity to deploy capital more freely in a variety of different directions. First, existing stores may receive an infusion of capital for store remodels and renovations. Second, closing stores may be less likely in the near term given the increase in demand. Third, there may be an increase in new store opens, though net new growth from many of the larger chains (e.g., Kroger, Albertsons, Publix, Walmart, etc.) may remain somewhat limited, but new units from growing chains could ramp. Finally, retailers will likely be able to accelerate digital initiatives, which include the build-out of online platforms and fulfillment for delivery and pickup.

Online share of food spikes… As a result of the pandemic, the online share of food and alcohol sales spiked in early 2020 to 11.2% from 3.6% in 2019, compared to pre-COVID-19 2020 estimates of ~4.4%. The online share of food and alcohol spend may fall back to the low-5% level, but there has been a significant step-change in the way consumers shop for food that could endure.

…But the stores still matter—they’re logging the majority of the online grocer sales. Despite the uptick in online spend for food and alcohol, Ms. Wein estimates that 95%+ of online food is fulfilled locally at the store, and she does not anticipate a significant shift in the years ahead. Retailers are in the process of building out both CFCs, or Centralized Fulfillment Centers (300ksf+), and MFCs, or Microfulfillment Centers (5-35ksf), to increase efficiencies across the supply chain and better handle online order fulfillment. Retailers appear to be working on building out networks that include both CFCs and MFCs. MFCs can be installed inside an existing store (likely a store with average or below-average sales) or at an entirely new location either at a retail center or flex/industrial facility. Moreover, Ms. Wein sees a strong possibility that MFCs in some locations may be integrated to service more than one retailer (e.g., grocery,

pets, office, etc.) at certain centers.

Notably, MFCs can backfill vacant space and/or hard-to-lease “elbow space” in certain centers, a trend that may accelerate given the increase in bankruptcies more recently. Comments suggest the timeline to build out an efficient network of CFCs and MFCs to “blanket the country” could be 24-36 months, though that seems aggressive, in our view.

There will be closures; the large landlord advantage. Retailers will continue to reposition store fleets, and there will be store closures in the near and long term, though there may be far less vulnerability of closures today given the increase in grocery spend taking place; the addition of CFCs and MFCs may also lead to store closures if retail space requirements decrease as a result. However, Ms. Wein expects larger landlords to maintain a significant advantage over smaller/individual shopping center owners (ownership within the open-air shopping center industry is extremely fragmented) that should lead to far fewer closures than smaller/individual property owners given: 1) better access to capital for funding TI and sharing in the build-out of MFC networks; 2) bigger portfolios with more locations to facilitate a faster rollout; and 3) higher-quality centers in stronger locations.

Malls may see some demand, but don’t expect a flurry of mall-based grocery activity. Despite recent commentary in the mainstream media and on mall REIT earnings calls, Ms. Wein thinks grocery will maintain its presence predominantly in open-air shopping centers. That said, there may be an incremental increase in grocery leasing at malls, particularly given the number of department store closures scheduled to take place in the quarters ahead, though it could be a more selective site selection process overall compared to what some may be anticipating.